Jewelry Care Insurance Options Protecting Your Investment

Explore jewelry insurance options to protect your investment. Understand the different types of coverage and how to choose the right policy.

Explore jewelry insurance options to protect your investment. Understand the different types of coverage and how to choose the right policy.

Understanding Jewelry Insurance Why You Need It

Let's face it, jewelry isn't just pretty; it's often a significant investment. Whether it's a bespoke piece designed with love, a high jewelry creation passed down through generations, or even a trendy everyday accessory, losing it, damaging it, or having it stolen can be devastating, both emotionally and financially. That's where jewelry insurance comes in. Think of it as a safety net for your precious pieces, offering peace of mind and financial protection against unforeseen circumstances.

Types of Jewelry Insurance Policies What's Covered

Navigating the world of jewelry insurance can feel overwhelming, but understanding the different policy types is key. Here's a breakdown:

- Homeowners or Renters Insurance: While your existing homeowner's or renter's insurance policy might offer some coverage for jewelry, it's often limited. The coverage amount is usually capped, and the deductible can be quite high. Plus, filing a claim can increase your overall premium. It's a good starting point, but rarely comprehensive enough for valuable pieces.

- Standalone Jewelry Insurance Policy: This is a specialized policy specifically designed for jewelry. It offers broader coverage and often includes benefits not typically found in homeowners policies. Think of it as dedicated protection for your bling.

A comprehensive jewelry insurance policy typically covers:

- Loss: If your jewelry is lost or misplaced, the policy will cover the cost of replacement or the appraised value.

- Theft: Protection against theft, whether from your home, while traveling, or even during a robbery.

- Damage: Coverage for accidental damage, such as a chipped stone, a broken clasp, or a bent setting.

- Mysterious Disappearance: This covers situations where your jewelry vanishes without a clear explanation. It's a crucial feature, especially since jewelry can sometimes just disappear!

Appraisal and Documentation Getting Your Jewelry Ready for Insurance

Before you can insure your jewelry, you'll need to get it appraised by a qualified gemologist or appraiser. An appraisal provides an accurate valuation of your piece, which is essential for determining the coverage amount. Make sure the appraisal includes a detailed description of the jewelry, including:

- Type of Jewelry: Ring, necklace, earrings, etc.

- Metal Type: Gold, platinum, silver, etc.

- Gemstone Details: Type, carat weight, cut, clarity, and color.

- Overall Condition: Any existing flaws or imperfections.

- Photographs: Clear, high-quality photos of the jewelry.

Keep the appraisal in a safe place, along with any original purchase receipts and certificates of authenticity. These documents will be crucial when filing a claim.

Factors Affecting Jewelry Insurance Premiums Understanding the Costs

Several factors influence the cost of your jewelry insurance premium:

- Value of the Jewelry: The higher the appraised value, the higher the premium.

- Coverage Amount: The amount of coverage you choose will directly impact the premium.

- Deductible: A higher deductible will typically result in a lower premium, but you'll pay more out-of-pocket if you file a claim.

- Location: Your location can affect the premium, as some areas have higher rates of theft.

- Security Measures: Having a home security system or storing your jewelry in a safe can sometimes lower your premium.

Choosing the Right Jewelry Insurance Policy Tips and Considerations

Selecting the right jewelry insurance policy requires careful consideration. Here are some tips:

- Read the Fine Print: Carefully review the policy terms and conditions to understand what's covered and what's excluded. Pay close attention to any limitations or exclusions.

- Replacement vs. Cash Value: Determine whether the policy offers replacement coverage (which pays for a brand new replacement) or cash value coverage (which pays the depreciated value of the jewelry). Replacement coverage is generally preferred.

- Worldwide Coverage: If you travel frequently, ensure the policy provides worldwide coverage.

- Ask About Exclusions: Clarify any exclusions, such as damage caused by normal wear and tear or pre-existing conditions.

- Compare Quotes: Get quotes from multiple insurance companies to compare coverage and premiums.

Real-Life Scenarios and Jewelry Insurance Coverage Examples

Let's look at some scenarios to illustrate how jewelry insurance works:

- Scenario 1: Lost Diamond Earrings

You're attending a gala, and after a night of dancing, you realize one of your diamond earrings is missing. With jewelry insurance, you can file a claim to have the earring replaced based on its appraised value.

- Scenario 2: Stolen Engagement Ring

Your home is burglarized, and your engagement ring is stolen. Your jewelry insurance policy will cover the cost of replacing the ring, ensuring you can find a new symbol of your love.

- Scenario 3: Damaged Gemstone

You accidentally bump your sapphire ring against a hard surface, chipping the gemstone. Your insurance policy will cover the cost of repairing or replacing the damaged sapphire.

Recommended Jewelry Insurance Providers

While I cannot endorse specific providers, here are a few well-regarded jewelry insurance companies you can research:

- Jewelers Mutual: A specialized insurer focused solely on jewelry.

- Lavalier: Another dedicated jewelry insurance provider with customizable policies.

- BriteCo: Offers instant online jewelry insurance with monthly payment options.

Remember to compare quotes and read reviews before making a decision.

Cost Examples and Policy Details

To give you a better idea of pricing, let's consider a few examples:

- Example 1: Diamond Engagement Ring (Value: $10,000)

A standalone jewelry insurance policy might cost between $100 and $200 per year, with a $100 deductible.

- Example 2: Pearl Necklace (Value: $5,000)

A standalone jewelry insurance policy might cost between $50 and $100 per year, with a $50 deductible.

Keep in mind that these are just estimates, and the actual cost will vary depending on the factors mentioned earlier.

Alternative Insurance Options and Add-ons

Some insurance companies offer add-ons to their jewelry insurance policies, such as:

- Inflation Coverage: This adjusts the coverage amount to account for the increasing value of your jewelry over time.

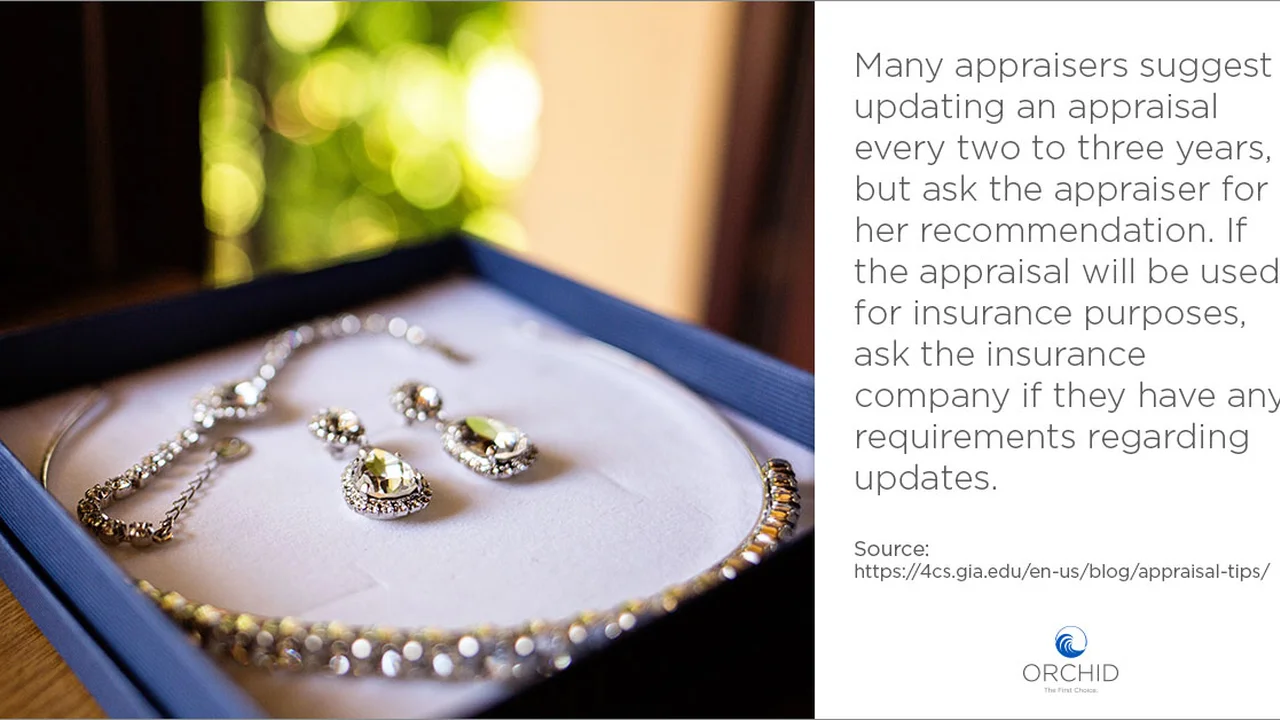

- Appraisal Updates: Some policies cover the cost of periodic appraisal updates to ensure your jewelry is adequately insured.

Practical Tips for Protecting Your Jewelry Beyond Insurance

While insurance is essential, taking proactive steps to protect your jewelry can minimize the risk of loss or damage:

- Store your jewelry in a safe place: Consider a home safe or a safety deposit box at a bank.

- Remove jewelry during activities that could cause damage: Take off rings before cleaning, gardening, or exercising.

- Have your jewelry professionally cleaned and inspected regularly: This can help identify loose stones or worn settings before they become a problem.

- Keep detailed records of your jewelry: Include appraisals, purchase receipts, and photographs.

Final Thoughts on Jewelry Insurance

Jewelry insurance is an investment in peace of mind. By understanding the different policy types, coverage options, and factors affecting premiums, you can choose the right policy to protect your precious pieces and ensure they're safeguarded against the unexpected. Don't wait until it's too late – take the time to explore your insurance options today.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)